The International Monetary Fund is headquartered in Washington in 2018. (Yuri Gripas / Reuters)

But are the countries allegedly trying to help?

As last week’s meeting of the G20 finance ministers in Venice, Italy, ended, there was one big winner: the International Monetary Fund (IMF). Undercover to assist the Parties in their efforts to fund efforts to alleviate COVID, The IMF will issue $ 650 billion Special Drawing Rights (SDRs). This is amazing 120 percent increase the stock of outstanding SDRs. They will be distributed to 190 IMF member countries in proportion to their quotas.

SDRs are a reserve asset – something like “paper gold” – to use a contradictory description – created from the air by the IMF. They were first issued in 1969, when IMF experts feared a shortage of international reserves and a shrinking liquidity that would lead to global deflation. However, as is often the case, experts are wrong. Since 1969, there has been an explosion in world reserves through the accumulation of US dollars from foreign countries. Contrary to experts’ expectations, SDRs proved to be insignificant in this respect.

But that hasn’t stopped IMF bureaucrats from trying to find ways to make SDRs “useful” so that the fund can produce more of them and expand the scope and scale of its operations. No one to let the crisis fall, the IMF is using the COVID pandemic to inflict gold.

How exactly do SPTs work? They are a basket of five currencies – the Chinese yuan, the US dollar, the euro, the yen and the British pound – which are used as a unit of account by the IMF. In addition, SDRs are interest-bearing assets that can be exchanged for cash, with the IMF facilitating the exchange of SDRs for cash between member countries. So SDR holders can potentially transform them into money if they find partners who are willing to participate in the exchange.

The significance of the $ 650 billion “gift” of free money to IMF member countries, blessed in Venice, is that an entirely new rationale was used to give life to the IMF’s special withdrawal rights – an asset mentioned in the past as a “great failure.”

This is not the first time that the IMF has rediscovered itself and snatched victory from the jaws of defeat. The IMF, which was born in 1944, is designed to provide short-term aid at cheap prices to countries whose currencies are pegged to the US dollar through the Bretton Woods agreement. When these countries find themselves in a currency shortage (ie US dollars), they could receive balance of payments assistance from the IMF. This was the initial, rather narrow task of the IMF.

But in 1971, when President Richard Nixon closed the golden window, Bretton Woods’ exchange rate system collapsed — sweeping the IMF’s original goal into the trash. Since then, the IMF has used every justification under the sun to rediscover and expand its scope and scale. Unlike the old soldiers, the IMF has not disappeared. He became even bigger and even more powerful. In this way, it became more political.

First, there were the oil crises of the 1970s, which allowed the IMF to quickly rediscover itself. These shocks are said to “require” more lending from the IMF to facilitate, yes, balance of payments adjustments. And there was more lending. In real terms, adjusted for inflation, IMF loans doubled from 1970 to 1975 and increased by 58% from 1975 to 1982.

With the election of Ronald Reagan in 1980, it seems that the opportunism driven by the IMF crisis will finally be brought under control. However, with the onset of the Mexican debt crisis, the political elite said more IMF loans were needed “to prevent financial contagion, more widespread debt crises and bank failures.” “Surprisingly, President Reagan accepted this well-founded and personally lobbied 400 of the 435 congressmen to get approval to increase the US quota (capital contribution) to the IMF. IMF loans rose again, rising by a staggering 27 percent in real terms during the first four years of Reagan’s rule.

And then came the 1990s, a decade of explosive growth for the IMF. The collapse of communism provided an opportunity that was too good to be true. The currency crises in Mexico, Russia, Turkey, Brazil, Argentina and Asia have added fuel to the fire, allowing IMF firefighters to expand their balance sheets and create more jobs for boys. As the saying goes, the show goes on and on, with the IMF playing the role of a hydra.

While the IMF’s ability to survive and thrive on death would not surprise British historian K. Northcott Parkinson, author of the 1957 classic. Parkinson’s law, this is quite remarkable in light of the actual performance of the IMF. Like Robert Barrot of Harvard University put it on, The IMF reminds him of Ray Bradbury’s Fahrenheit 451 “In which the fire department’s mission is to light fires.” Barrot’s basis for this conclusion is his extensive research. His damn evidence establishes this

- higher participation rate in IMF loans reduces economic growth;

- IMF lending reduces investment; and

- greater participation in IMF programs lowers the rule of law and democracy.

And if that’s not bad enough, countries that participate in IMF programs are usually recidivists. In short, IMF programs do not provide treatment, they create addicts.

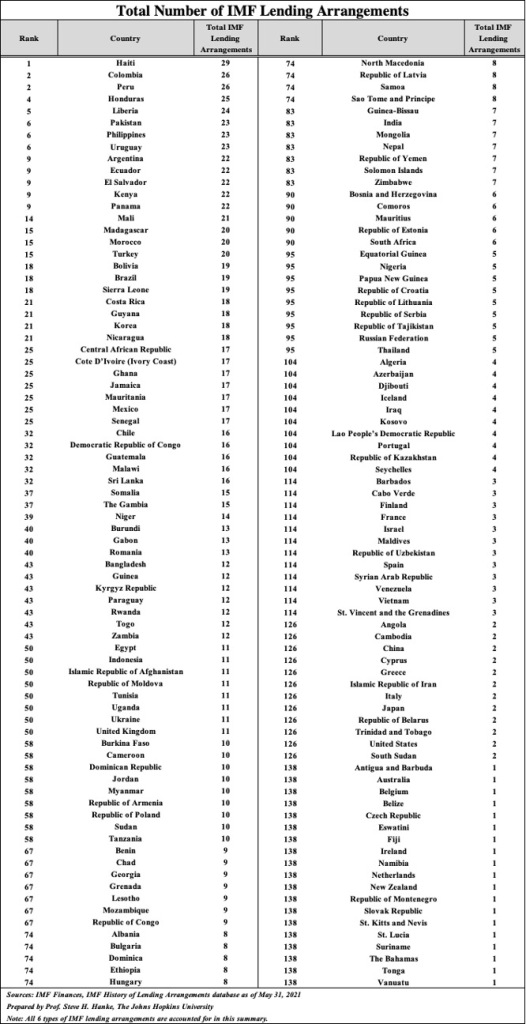

For a clear idea of the extent of this problem, see the table below. He lists the number of IMF programs in which 156 countries have participated. Haiti leads the group with 29 programs. Since joining the IMF in 1953, the country has averaged about 2.3 years between new IMF programs. Argentina is another heavy striker. He joined the IMF in 1956 and is now included in his 22nd IMF program. This is a new program on average every 2.9 years. More broadly, the list of countries with the ten largest credit programs (including links) consists of 24 countries. These countries account for 36 percent of the total number of IMF loan packages, indicating an alarming pattern of relapse.

The IMF has long been to be wiped out and placed in a museum. After all, its original function was abandoned in 1971, and its performance in new ventures is less than stellar. But there is no museum for the IMF in the maps. Even the reform is hard to imagine. In fact, all attempts to reform and reduce the IMF have ended in expanding its scope and scale. Just look at what has been achieved since 2000, when the blue ribbon International Financial Advisory Committee – chaired by my good friend, the late Alan Melzer – recommended the IMF to be controlled.

All we can do is realize that the IMF is a political hydra with a program that satisfies the bureaucrats it employs and serves the desires of the political elites that allow it to raise new heads.