Contrary to economists’ expectations for the sixth month in a row, inflation is warming instead of weakening. And that’s a lot worse than it looks.

From Wolf Richter for WOLF STREET.

The consumer price index jumped 0.9% in June since May, after jumping 0.6% in May and 0.8% in April – all of them the steepest monthly jumps since 2009, according to Bureau of Labor Statistics today. The CPI excluding volatile food and energy components (“core CPI”) jumped 0.8% for the month and 9.5% for the last three months, the hottest “CPI core” since June 1982.

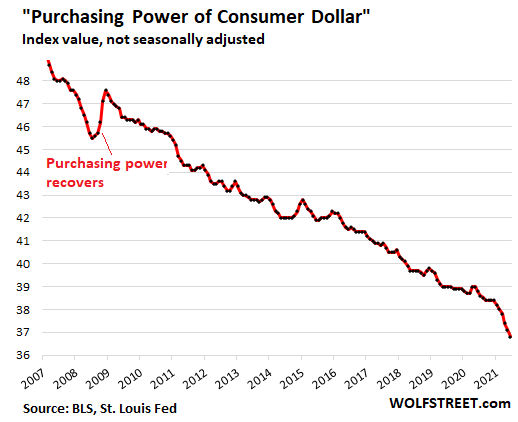

On an annual basis, including periods of low inflation last fall, the CPI jumped 5.4%. The CPI tracks the loss of purchasing power of the consumer dollar – everything denominated in dollars for consumers, including what they can buy with their labor – and this dollar has fallen by 10.7% in the last three months a year, the fastest decline since June 1982

The loss of purchasing power is “permanent”, ands shows the diagram.

There is nothing “transient” or “temporary” in the loss of purchasing power, as the chart above shows. Only a period of deflation can change part of the decline in purchasing power, which is a rare event in the United States and happened only a few quarters of my life, including a few months in 2008 – this small gap in the chart above.

The only aspect of inflation or the loss of the purchasing power of the dollar that is temporary is the speed at which it progresses, faster or slower, from month to month.

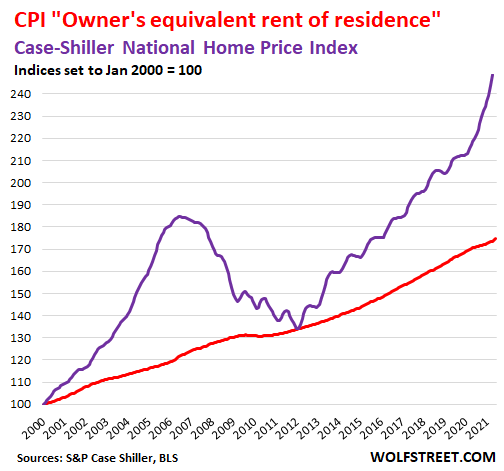

Actual jumps in house prices against the CPI housing charade.

Housing costs – rental and property costs – are included in the CPI as services and represent about one third of the total CPI. This is the largest, but barely moving despite rising housing costs.

The rental component of the CPI (“main dwelling rent”), weighing 7.7% of the total CPI, is growing every month this year by a constant 0.2%, including in June, and is only 1.9% on an annual basis.

The home ownership component (“equivalent rental of owner-occupied dwellings”), weighing 23.7% of the total CPI, rose 0.5% in June and only a staggeringly low 2.3% year-on-year, despite from how house prices explode, no matter how they are measured.

The average price of all types of existing housing in the United States, as tracked by the National Brokers Association, jumped by a record 24% compared to a year ago.

The Case-Shiller home price index, which measures changes in prices over time the same house and is therefore an appropriate measure for housing price inflation, jumped 14.6% year on year, the hottest data growth since 1987. (purple line). This contrasts with the volatile CPI for home ownership (red line):

The reason why the CPI’s property component does not track this frantic inflation in house prices, and thus the loss of the purchasing power of the dollar relative to homes, is that it does not track it. It is based on research and tracks what homeowners think their home might have Rent for – hence its name, “equivalent rent of owners’ homes”. This is a measure of rent, as imagined by the homeowner.

Hotels and motels. Rental and home ownership measures are the dominant components of shelter. The small components are “accommodated away from home”, which is mainly hotels and motels, weighing 0.9% of the total CPI. So they are not big. But prices jumped 7.9% in June and 16.9% year on year.

So maybe the prices of hotel rooms just catch up where they were. And for city hotels that are just returning and still suffering from a lack of business tourism, this is one of the factors. But hotels that serve tourists for leisure, especially in recreation areas such as around national parks, have been booked well and prices have skyrocketed.

The CPI for services, which is dominated and statistically controlled by the upper charade of housing inflation, reached 0.4% in June and 3.1% on an annual basis.

Durable goods inflation jumped 14.6%, the highest since at least the 1950s.

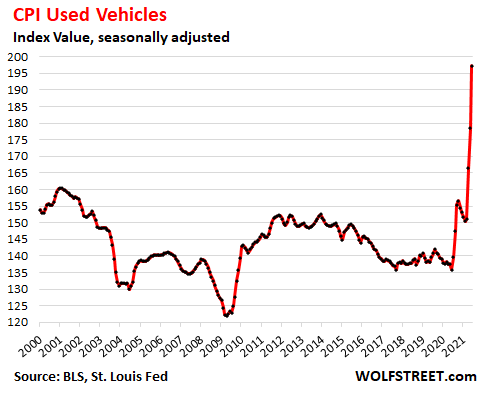

Durable goods, which include cars and trucks, appliances, consumer electronics, furniture and the like, rose 3.5% in June from May and 14.6% year-on-year, the biggest jump in data dating back to 1957 The jump is fueled by the prices of used and new vehicles.

The consumer price index of used vehicles has exploded by 45% on an annual basis, and by 10.5% in June. For months I have been documenting this madness, which cannot and will not continue and which will at some point be partially relaxed. And now there is the first signs from wholesalers that this is finally “Peak Insanity” in used cars and especially used trucks. Clearly, part of this ridiculous jump in CPI for used cars and trucks is “transient.”

Long-term price increases are crushed by “hedonic quality adjustments”. As you can see in the CPI chart of used vehicles, the prices of used vehicles seem to have fallen in the 1920s between 2000 and early 2020, which is, of course, a ridiculous statement. The prices of used cars and trucks have obviously jumped during these 20 years.

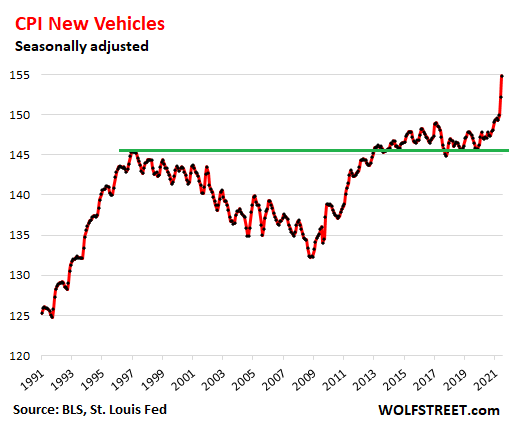

But the Bureau of Labor Statistics uses “hedonic quality adjustments” to account for improvements in vehicles over the years (for example, from a four-speed automatic transmission to a 10-speed electronically controlled transmission). Price increases expected to be associated with “quality improvements” are removed by the CPI for new and used vehicles (hedonic quality adjustments explained here with my real two-year F-150 and the Camry vs. CPI price index for new vehicles).

The idea is that the CPI measures changes in the prices of the same item over time; and when the item improves, it is no longer the same item and the price increase is not inflation because it reflects a better product. In fact, this has led to a consistent, targeted and very bilateral reduction in inflation as measured by the CPI. Same as housing data. The idea is to keep people in the dark.

The CPI of the new vehicle takes off. In June, the consumer price index for new cars and trucks jumped 1.8%, after jumping 1.5% in May, the biggest jump since a month since the launch of the cash program during the Great recession. The index is now growing by 5.3% on an annual basis. Even the aggressive application of hedonic quality adjustments that pushed the new vehicle CPI, even when vehicle prices have actually risen, cannot cope with these price increases:

What to make of it.

There are completely underestimated components in the inflation data today, such as housing inflation, which is actually hot. And there are temporary factors, such as the jump in used vehicles that cannot continue. Price increases are spreading to other categories.

What we will see in the future are ups and downs in the monthly rate of inflation, which will give false hopes of reducing inflation, followed by increases that destroy those hopes. And we still do not see the real rate of inflation due to the improper inclusion of housing costs and due to other strategies, such as the overly aggressive application of hedonic quality adjustments. So inflation is here, both high and low, but it will change up and down every month.

Meanwhile, the Fed is still buying $ 40 billion a month in mortgage-backed securities, thereby repressing mortgage interest rates, doing everything possible to further heat up housing inflation, and still buying $ 80 billion in government securities per month and it maintains its interest rates close to 0% to suppress short-term and long-term interest rates in general and inflate asset prices and consumer prices, thus further burning the purchasing power of the dollar.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I completely understand why – but I want to maintain the site? You can donate. I appreciate it extremely. Click on the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()