Are central banks annoyed by the drunken stamp of money from the Fed and the giant debt of the US government? But still a mocking Chinese renminbi.

From Wolf Richter for WOLF STREET.

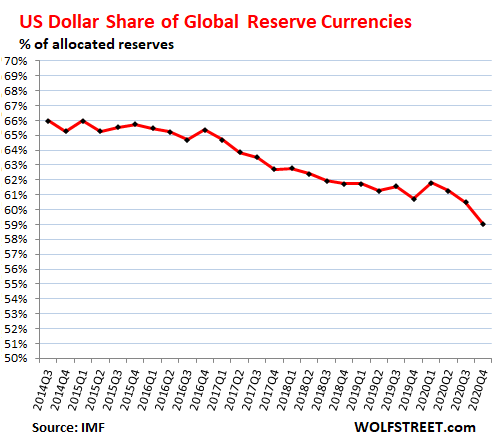

The global share of US dollar-denominated foreign exchange reserves fell to 59.0% in the fourth quarter, according to IMF COFER data released today. This corresponds to the 25-year low since 1995. These foreign exchange reserves are government securities, US corporate bonds secured by mortgage-backed securities, commercial mortgage-backed securities, etc., held by foreign central banks.

Since 2014, the share of the dollar has fallen by 7 full percentage points, from 66% to 59%, by an average of 1 percentage point per year. At this rate, the share of the dollar will fall below 50% in the next decade:

The foreign exchange reserves do not include the Fed’s own holdings of dollar-denominated assets, its $ 4.9 trillion in U.S. securities and $ 2.2 trillion in mortgage-backed securitiesthat it has accumulated as part of QE.

The status of the US dollar as the dominant world reserve currency is a decisive factor for The US government continues to bubble with its public debtand for Corporate America’s continued efforts to create huge trade deficits by directing production to cheap countries, most prominently China and Mexico. They all rely on the willingness of other central banks to hold large sums denominated in dollars.

But it seems the central banks are a little nervous and want to diversify their holdings – but still so slowly and not suddenly, given the size of this thing, which, if handled incorrectly, could blow the house of all cards.

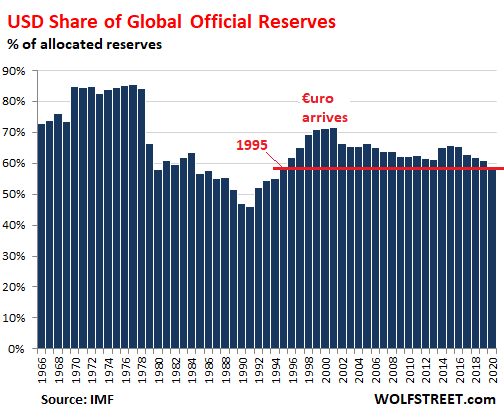

20 years of decline.

Two decades ago, when the dollar had a share of about 70% of reserve currencies, a supposed competitor became an everyday reality: the euro, which combines Member States’ currencies into one currency, thus combining their weight as a reserve currency. Since then, the dollar has fallen 11 percentage points.

In contrast, between 1977 and 1991, the share of the dollar fell by 46 percentage points – with huge declines in 1979 and 1980, probably due to US inflation, which threatened to spiral out of control, reaching a peak of nearly 15 % in 1980 in 1991, with inflation more or less under control. And then the share of the dollar rose by 25 percentage points by 2000:.

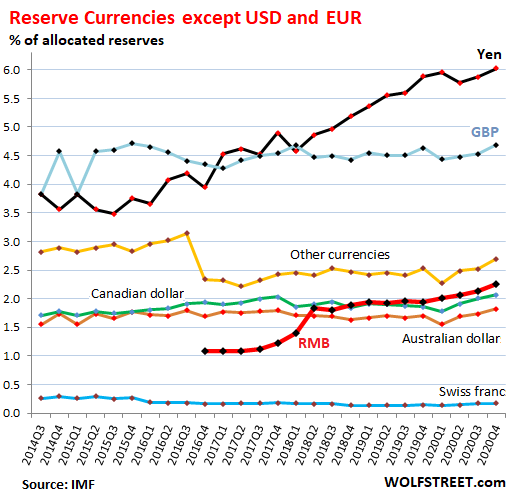

Other reserve currencies.

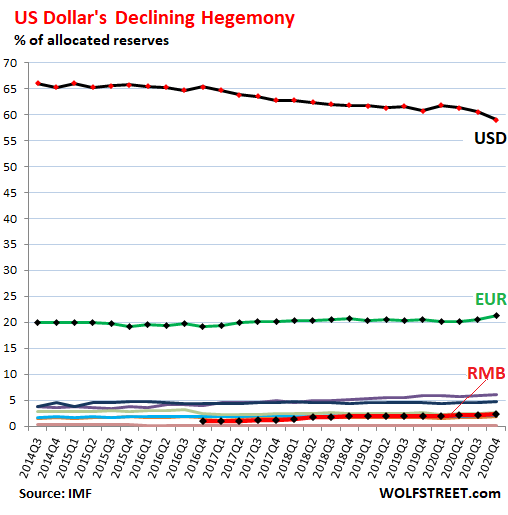

Since then, the euro’s share has ranged between 19.5% and 20.6%, but in Q4 it went out of range and rose to 21.4%, the highest in the data. The ECB’s holdings of euro-denominated assets that it has acquired as part of QE are not included in euro-denominated foreign exchange reserves.

The other reserve currencies are also rans – the spaghetti below in the table below. This includes the Chinese renminbi, the bold red line at the bottom:

Zhenminbi a threat to the hegemony of the dollar? Not yet.

The share of the yuan is still only 2.25%, despite the scale and global influence of the Chinese economy and despite the noise when the IMF raised the yuan to the official global reserve currency in October 2016, including it in the basket of currencies that support the special Drawing rights (SDRs).

But the share of renminbi is growing so slowly. At the pace that has been gaining momentum over the last two years (+ 0.36 percentage points in two years), it will take another 50 years for the renminbi to reach a 25% share.

It is obvious that other central banks are still interested in the renminbi and its consequences and are reluctant to charge their dollars at once in exchange for the renminbi; makes it easy.

Also – under the microscope: Raising the yen.

To see what happens to the spaghetti at the bottom of the chart above, I zoomed in and limited it to 0% to 6%. This removes the dollar and the euro from the picture and allows a detailed overview of other reserve currencies.

What stands out is the jump in the yen, the third-largest reserve currency. This includes 2.0 percentage points profit from Q4 2016, which was 1.15 percentage points for the same period of renminbi. With regard to the yen, the renminbi is losing ground.

Despite Brexit and all the terrible insults around it, the pound sterling (GBP), the fourth largest reserve currency, did not give up any share.

The euro area has had a large trade surplus – between € 200 billion and € 275 billion a year in recent years – with the rest of the world since emerging from the euro’s debt crisis in 2012. The US trade deficit with goods with the euro area was 183 billion dollars in 2020..

The euro area’s trade surplus shows that it is easy for an economic area with a large trade surplus to also have one of the best reserve currencies. There is no requirement for a large reserve currency to be associated with a large trade deficit. But having a dominant reserve currency is helping the United States finance its trade deficit and increase government debt.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I completely understand why – but I want to maintain the site? You can donate. I appreciate it extremely. Click on the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()